Valve’s latest update on the Steam Machine is being framed as good news: the company now expects to fulfill all current reservations by the end of 2026 while continuing to ramp production. On its face, that sounds like evidence of overwhelming demand, but I’m not convinced the reservation queue tells the whole story. A reservation is a low-cost expression of interest, not a purchase commitment. Some people joined simply to watch how the process unfolds, others are waiting to see whether pricing changes, and the existence of Steam Machines already appearing for resale above MSRP strongly suggests that scalpers are participating as well. That doesn’t mean demand isn’t real; it simply means the reservation queue is an imperfect measure of genuine consumer demand.

The pricing reinforces that skepticism. Unlike the Steam Deck, which was priced to attract a broad audience, the Steam Machine occupies a much narrower niche. At well over a thousand dollars, it isn’t an impulse purchase or an easy recommendation for the average gamer. In fact, I still believe market demand is well below the optimistic projections some enthusiasts have floated and likely below the demand profile the Steam Deck enjoyed. Today’s buyers are far more likely to be Linux enthusiasts, PC hardware aficionados, or gamers with a very specific interest in SteamOS than casual players looking for an alternative to an Xbox or PlayStation. That doesn’t make the product unsuccessful; it simply defines the limits of the audience Valve is serving today.

Ironically, the long reservation queue may become more meaningful if the broader PC hardware market shifts. As GPU prices continue to rise and memory and storage remain under pressure from AI-driven demand, a prebuilt Steam Machine could become a more attractive alternative for some gamers than assembling a new gaming PC. While I expect a number of reservation holders will ultimately decline to purchase when their place in line arrives, those units are unlikely to sit idle. If demand for premium gaming hardware remains healthy, other buyers, including resellers hoping to capitalize on limited availability (scalpers), will almost certainly absorb much of that excess inventory.

The more important story, however, has very little to do with reservation counts. Valve has already put its foot in the door with SteamOS hardware, and backing away now would send exactly the wrong signal. The company needs to demonstrate consistency, commitment, and confidence; not simply to consumers, but to potential hardware partners. SteamOS will only become a mainstream platform if major OEMs such as ASUS, Acer, Dell, HP, Lenovo, Samsung, and others believe Valve is committed to supporting it for the long haul. Those manufacturers possess purchasing power and supply-chain advantages that Valve simply doesn’t have, allowing them to build SteamOS-powered systems at more competitive prices once they believe the ecosystem has staying power.

In that sense, Valve’s promise to fulfill reservations by the end of the year is less about selling every Steam Machine itself and more about proving that SteamOS is a platform worth investing in. The company’s decision to release the Steam Machine’s enclosure CAD files under a Creative Commons license reinforces that philosophy by encouraging community involvement while signaling that SteamOS is intended to be an open ecosystem rather than another closed console. If Valve can maintain that commitment, convince OEMs to build compelling SteamOS hardware, and capitalize on the still underdeveloped mini-PC market, today’s relatively niche product could become the foundation for something much larger tomorrow. The Steam Machine itself may never dominate the gaming market, but it doesn’t have to. Its greatest success may be proving that SteamOS deserves a permanent place in the PC hardware landscape.

Microsoft has responded to reports that some Xbox players were unable to launch even physical disc-based games during a recent Xbox Live outage, acknowledging that this behavior was unintended. According to the company, consoles should have relied on locally cached licensing entitlements instead of requiring an online validation check, and Xbox says it is investigating the issue while preparing a software update to prevent it from happening again. What’s particularly interesting, however, is that this is the second time in roughly the last three years that Microsoft has pointed to cached entitlement handling as part of the root cause for a major outage. That raises legitimate questions about the complexity of Xbox’s licensing architecture, even if the immediate bug is ultimately straightforward to correct.

What struck me most about the reaction to this story wasn’t Microsoft’s explanation, it was the familiar chorus claiming that this somehow proves physical media is inherently superior to digital distribution. That conclusion simply doesn’t hold up. People continue to conflate three completely different concepts: the storage medium, the delivery mechanism, and the licensing system. A Blu-ray disc, a downloaded game stored on an SSD, and virtually every other modern game installation are all just data written to physical storage. The real question isn’t whether the installation files arrived on a disc or over the internet. The question is whether the game depends on online entitlement validation or server-side functionality to operate. If a game requires a “hello world” check-in with a licensing service, or worse, relies on live server infrastructure for gameplay, even a physical disc cannot insulate you from a network outage.

This is why I think discussions surrounding both the recent Xbox outage and earlier PlayStation Network outages have missed the point. Modern gaming ecosystems are deeply integrated with online identity management, entitlement services, cloud infrastructure, and, in some cases, server-hosted gameplay systems. Ubisoft’s The Division 2 is a perfect example: even if you’re playing alone, portions of the game’s functionality still rely on server-side systems.

Whether you purchased that game digitally or on a physical disc becomes largely irrelevant once the game’s architecture depends on online services. The same principle applies to platform licensing. When cached entitlements work correctly, offline play should continue uninterrupted for games that don’t require server-side functionality. When they don’t, both digital purchases and physical discs can be affected in exactly the same way.

None of this excuses Microsoft. If anything, the recurrence of cached entitlement issues suggests that Xbox’s licensing infrastructure may be more complicated & fragile than many people realize, likely reflecting the company’s extensive integration with Azure-based identity and entitlement systems. At the same time, I think the public conversation often exaggerates the scale of these outages. Over the last several years, we’ve seen only a handful of significant incidents measured against thousands of days of service. Five-nines reliability still allows for occasional failures, and no cloud service offers 100 percent uptime. Rather than promising perfection, Microsoft, and Sony, for that matter, would serve players better by demonstrating continuous investment in reliability. Quarterly engineering updates highlighting infrastructure improvements, capital investments, regional capacity expansions, DevOps / SRE initiatives, or resiliency enhancements would do far more to build confidence than only communicating after an outage has already occurred.

Ultimately, I don’t believe this incident strengthens the argument for physical media nearly as much as some commentators suggest. Instead, it highlights a broader reality about modern gaming: ownership, licensing, authentication, and online infrastructure are now tightly intertwined regardless of how the software was delivered.

Physical discs are no longer a guarantee of complete independence from network services, just as digital purchases are not automatically at risk every time an outage occurs. The lesson from this outage isn’t that discs are the future or that digital distribution is broken. It’s that platform holders must continue investing in resilient entitlement systems, transparent engineering practices, and robust offline functionality so that the rare network outage remains exactly what it should be: a temporary inconvenience rather than a defining characteristic of modern gaming.

I bought the first Xbox on Day 1. My first run of the Halo campaign was in co-op with a buddy of mine who was out on the West Coast over Thanksgiving. Bought the 360 right before moving and took it on the road with me. Bought a little 20″ Polaroid 1080i TV so I could play in my apartment while I waited for my stuff to be delivered. On the launch of the Scorpio, I had three launch day units because I’d ordered from 2 different vendors on Amazon, and another one from Best Buy. I’ve had a Series S and a Series X. PC has been my preferred platform overall for almost 30 years, but Xbox was my preferred console for gens 6, 7, and 8.

As a kid, and before I was multiplat, I was Sega. Had the Master System, Genesis, Saturn, & Dreamcast. I lived through their exit of HW. I lived through the vanishing of the gaming market in North America from 1983 – 1985. I’ve seen Atari, Intellivision, Colecovision, Magnavox, Neo Geo, 3DO, TurboGrafx, Phillips CD-i, and probably others come & go.

I’ve spent money on Xbox for almost 3 decades. But Xbox is responsible for making Xbox go. And since 2020, they have tried to make Xbox go on influencers and content creators and a lot of distraction rounds & decoys and it has not changed with this new regime. If Xbox had raised Game Pass Ultimate to $30, dropped it to $23, paywalled Day & Date, and pulled CoD, I would have said the same thing about it I do when PlayStation does stuff. “That’s just business and consumers will decide if it is acceptable or not”.

But they tried a lot of smoke & mirrors and fired a lot of decoy & distraction rounds in doing all of that, which is what the past 6 years have been. I have umbrage because Xbox has been on this pogrom of pandering, placation, and appeasement. Trying to play the good-guy routine in order to get a pass on its deliverables. PlayStation and other vendors tend to just say “This is the product, here is my price” and listen to how the market responds or doesn’t with money. It’s not a reality TV show like it is with Xbox.

I do not care about Game Pass, Play Anywhere, This is an Xbox / Everything is an Xbox, Cloud, Smart Buy, Cross Buy, Velocity Architecture, Xbox FanFest, FanFest World Tour, logos and boot-up screens. Because what goes hand-in-hand with that is all of the “exclusives are antiquated”, now “we need exclusives”, “you might need to upgrade your PC” to play Starfield, “Redfall is a miss but we’re seeing good engagement in Game Pass so how big a miss is it?” and other Greatest Hits of their PR and marketing. IMO Xbox needs to STFU and focus on providing me great games, and I have not played a Great Xbox game since last gen. I loved Avowed, and South of Midnight, but those things did not shake the earth.

Fable is the first thing of that ilk IMO in a long time. I am not here for XBox stuff that they have been doing for 2.5 decades re-dressed. Zero interest in Gears E-Day. Zero interest in Halo: Combat Evolved. I’ve played that campaign a half-dozen times.

For me they need to move the needle and the art forward. I only care about exclusives if they allow teams to code close to the metal, keep the dev cycle tight and minimize defects, extract the max from the singular HW set, & use the spare capacity to move the art & design forward. And focus on great performances. I, personally, do not see that in E-Day. Or Combat Evolved.

You have Ashley Johnson moving everyone to tears on the Naughty Dog set, making everyone have to take ten after the Joel scene on the mocap set for TLOU2. That’s what I am looking for from Xbox. They have the resources. There is no excuse.

If there is one thing that is true about internet gamers, it’s that they have a hard time minding their own business. There is way too much commentary on not understanding how or why other gamers game the way that they do. It doesn’t matter if someone likes revisiting the same 5 games that are their favorites, or whether they have a backlog that they glamorize like Gollum and the One Ring. It doesn’t matter if they can’t stand 30fps, love racing games, like GAAS games, open-world Assassin’s Creed games, play on PC, only want to play on console, or whatever else their chosen creed is.

While the platform-wars have established tell-the signs of someone being messy, others who consider themselves above the platform-war skirmishes are frequently equally as judgmental. There is this thing where in many ways online social media discourse about gaming is very centric to only the story-driven narrative stuff. And then they do not understand why a vast majority of the revenue generated on the market is from GAAS games. Or why certain genres have rabidly loyal communities. I think that it is because in their descent into being judgmental, they missed the ability to recognize the dynamics that motivate gamers other than ones that fall in their specific lane.

News flash. It’s not up to any individual gamer to need to “get” what motivates other gamers. And if you are a content creator, it’s fine that you don’t. But if you are trying to understand the market, then you really need to get out of your own way and try. And if you can’t do that, then, as Colin Moriarty says, it’s not necessary as a content creator for you to have an opinion on everything. It’s ok for you to sometimes just STFU and mind your own business and leave people TF alone.

There’s too many content creators who never come out of review mode. Like, when I am playing a multiplayer game, I don’t need your rolling commentary on why you want to give the game an IGN 7. I’m literally actively engaged in trying to have fun playing the game. And when I mention that I am playing a game, I also don’t need your opinion that you don’t think very highly of the game. Or that the game didn’t hold your interest. That you bounced off it. Maybe it wouldn’t pain you to do like we do on E2KG (shameless plug) and be curious about what the other person finds interesting about the game.

Maybe the truth is that content creators make great mutuals, but aren’t the best gaming friends.

Xbox lowered the price of Game Pass today. But the truth behind the facade is different than some will be lead to believe. While Call of Duty comes out of the service for the first year of any new version (by which time it will be value-less as the multiplayer community will have moved on to the next version), as the ostensible reason the price can be lowered, plenty of other useless content remains.

Do you still need:

Fortnite Crew

Ubisoft+ Classics (these games are frequently on sale for $4.99)

Benefits for CoD Warzone (when the cross-rewards earnable, Battle Pass, & store MTX are for the version of CoD that is now not in Game Pass)

They raised the price by $10, then reduced it by $7, and are voicetracking it as a good deal, as a means to obfuscate that they are keeping the extra $3 in their pocket. In order to spin it that they are the good guys.

This is because they were losing too much money by putting CoD in Game Pass. If it was really about GP having become too expensive for Gamers, they would have dropped the price to $20, and left a CoD tier that you could add as a kicker with an extra $5 to $6, and maybe added access to a WoW subscription or something else.

A thing that has not been talked about or given much specificity by the gaming media: as the COO at Instacart, one of Sharma’s major “accomplishments” at Instacart was dynamic pricing that tested to see how much people would be willing to pay for grocery items, and would set the price at the higher price people were willing to pay. Eversight, the AI company whose technology powered this strategy was acquired by Instacart in 2022. Asha Sharma’s tenure as COO was February 2021 to February 2024. Her specific purview included the implementation of this strategy, via her oversight of Instacart Marketplace, the consumer app, logistics, and engineering. Her specific mandate: guiding the company through its IPO and towards profitability. The settlement with the FTC found the following predatory practices:

Algorithmic “Smart Rounding” and A/B Testing

Price Disparity (75% of items with 23% price variance)

Targeted Markups for least price-sensitive items using “dynamically optimized pricing”

Hidden pricing deltas to specifically raise retailer revenue & profits

surveillance pricing

Not dynamic discounts, but actually setting higher prices. Costing a family of 4 as much as an additional $1200 per year. Of course, by the time of the investigation and hearings, she has already departed Instacart. But productization time and implementation of these functions, given the amount of time they would have taken to roll out to production and seen real returns at retailers, means the efforts would have had to have started during her tenure and within her purview. She was part of the leadership that pursued the Eversight acquisition to power the strategy, which Instacart had already started before. So a lot of what she talks about in using AI, while not for content-slop, her past history here shows how she believes in using it.

This is an incremental test to see how mcuh people are willing to pay. If the response of people coming back is not enough, more stuff will come out.

Additional case in point: Call of Duty went into the service in 2024 with no Game Pass price increase. When the sign-ups to Game Pass were not enough, and they could tell by summer of 2025 (after their financial year closed out and they’d collected all the data), then they raised GP prices as a result of the tepid response.

Seal-clubbing is a time honored tradition. It is the online digital gaming equivalent of hazing; of putting newbs on the frat pledge line and putting them through the ringer. In truth, it is much less “congenial” than that, if I can use that term even in reference to frat hazing (which tells you just how far down the rabbit-hole we are). It’s way more toxic than that. It is an “end justifies the means” approach of attacking newcomer players in a MMORPG who break out of the training zone (ganking). In the training zone, or security zone…each game calls it something different…there are typically steep penalties for attacking other players, if attacking other players is even allowed. Once that training period is over and players cruise beyond that mystical barrier, it’s no-holds-barred, falls count anywhere in the building. And players who have accrued better gear will pounce on any junior players foolish enough to travel alone. This has been a key element to the gameplay loop of EVE OnLine. And the result has been for the EVE community to form its own corporations, gangs, tribes, family businesses, etc, often with complex relationships and chains-of-command. But the main thing is that in exchange for pledging loyalty and the house taking it cut of any spoils, you gain mutual defense.

On April 14th, CCP Games launched EVE Online Exordium. A paraphrase of the blog post follows:

“Exordium is a new dedicated starter region aimed at improving the new player experience. Instead of spawning across scattered systems, all new players will…

…begin in this single 53-system region, making it easier to meet others, play with friends, and engage with corporations early on. The region is structured around a central hub system and dynamically assigns players to starter systems to keep populations balanced. It’s designed to reduce the confusion and isolation new players often feel, while also encouraging mentorship and social interaction between rookies and veteran players.

Exordium is intentionally a safe, low-risk learning environment where PvP is completely disabled, allowing newcomers to learn mechanics without fear of attack. To preserve balance, it features restricted content, lower rewards, higher taxes, and limits on advanced systems like player-owned structures. Activities are curated and scaled for beginners, with simplified resources and adjusted rewards to match early progression. Over time, players are expected to “graduate” out of Exordium into the wider, more dangerous universe, ensuring the region acts as a structured onboarding space rather than a permanent destination.”

While this is a great baby bottle to ease players in, my concern is that it doesn’t matter to the end result: that you need to join a larger corpo with greater resources so that you can have worthwhile defenders looking out for you. And the crimp that puts on people is that you have to make a commitment to the game that a lot of people won’t want to because they want to play more than just one game. This is a great improvement for those looking for that one main social community; or even just one amongst two or three tentpoles. But it does not hugely change the value prop for someone looking to add a new game to the rotation of 2 or 3 other games and does not want any one of them to be a full-time commitment.

I had some other thoughts for the title of this blog post:

“PC Parts Aren’t Disappearing—The Media Just Wants You to Think They Are”

“Fear Sells: How Games Media Helped Justify 100% PC Part Markups”

“Stop Paying Panic Prices: The Truth About DIY PC Costs Right Now”

“This Isn’t a Shortage—It’s a Narrative (And It’s Costing You Money)”

“From Journalism to Fearmongering: Why PC Prices Feel Out of Control”

Look. I’ve never been one to make a lot of noise about “anti-consumer”, “price-gouging”, or really just price increases in general. The market always seeks equilibrium between suppliers and buyers; you guys have heard that old saw from me a million times. No need to beat a dead horse.

What’s going on right now in DIY PC-land is pretty much a travesty. Let’s start with the games media. Quite frankly, whether it’s the PC market, console market, or just consumer electronics in general, I’ve kind of had it with the brain-rot headlines that have made up a recurring sensationalist wave these first four months of the year.

Literally every day, I see some multiple sites run a headline that “…so and so says umptyscrunch prices are likely to increase in the next x months”. About everything. SSDs. RAM. Power Supplies. Steam Machine. Project Helix. PS6.

And so what does this lazy journalism based on rumor, conjecture, speculation, gossip, and bullshit lead to? Today WCCftech ran a story discussing the current pricing of components at Microcenter. Let my accusation be clear: this egregious pricing is being enabled by the games and tech media + influencers with their nonsense. Tom’s Hardware is the only site I’ve seen (there may be more) who are running weekly price-checks of various component categories. Even as I say that I admit that I have not checked to see how valid they are, so dip there with your own cognizance. The rest of the games media are having weekend freelance bloggers run brain-dead assertions of a thing that is not happening, thereby enabling things that should not be happening.

For Microcenter, let’s walk this dog:

Microcenter => 2TB at $699

Amazon => $343.45

Microcenter => 128GB RAM kit at $4199

No one and everyone => no one needs 128GB of RAM so who give a s***?

Microcenter => 32GB of RAM at $699

Newegg => 32GB of RAM at $389

Even with the notion of there being a price premium for being able to procure locally, there is zero excuse for a 75 – 103% markup over similar-to spec’d components available from other retailers. Microcenter is doing this because they know now they can get away with it. And they know they can get away with it because of the idiotic fear-mongering going on in the games media and online. For months the media and wanna-be-relevant influencers have slaked off of the doomsday scenario that there’s nothing left and prices for components are in the 1000’s of dollars. They have also not revisited historical prices trends and depicted how RAM and SSD prices have moved over time. We’re only ten years into SSDs becoming priced to be the normalized pick for your boot drive, 5 – 7 years for capacity drives, and only 4- 6 years for picking nVME as the norm. Prior to each of those transition times, SSDs in either 2.5″ or nVME form-factor had not hit the affordability points to be the norm. And I’ve already covered the realistic view of RAM over the 30 years of past history.

I get that a lot of people who came into PC gaming when you could get 32GB of RAM for $82 are experiencing sticker shock. The does not excuse the lazy reporting, the doomsday extinction-level event story-telling, and the fabrication of a crisis that does not really exist. And of course @BRAP_Podcast just bought a perfectly performant gaming PC with an RTX 5080 for $2600 (actually I think he even got it marked down on sale).

Don’t buy into the BS. Check prices. Expect more of the games media. It’s pretty pathetic right now. But also, do not pay these ridiculous prices at Microcenter. Especially when the truth is they have plenty of stock. And yet are selling components at scalper and pirate prices.

Nope. This doesn’t make any sense. And it is exactly what I am talking about is part of the industry problem. What am I on about? Today, GameRant reported that Jason Blundell opened a new studio, Magic Fractal. This is the third studio he has opened in 5 years. None of which have shipped a game.

Before people go in on me thinking that I am making a dig at Blundell, that is not the case. I’m not putting him in the same bucket as I do Jade Raymond. My point is that, in 5 years, he has run into the adversity that the market, or at least PlayStation’s assessment of it, will not support whatever game he is working on, whether it be due to genre, content, or other factors. And that still applies if it has been different games that he pitched while at Deviation and then Dark Outlaw.

And that is not specific to PlayStation. And those market conditions will not change with Magic Fractal. The market still sends 19k games to Steam each year, 5700+ to consoles. The socioeconomic middle-class in the United States is getting squeezed with less discretionary income to put into video games spending. And there is more free content for the middle-class that they can partake of without spending any money on TikTok and YouTube, or with the allure of payouts in prediction markets (ie legalized digital gambling).

The industry needs fewer games. And less studios.

This penchant to spawn another independent studio when there are not enough people buying the AA and indie stuff. When the available funding in the games industry outside of the traditional publisher pipelines has become radically more scarce post-pandemic. And when those traditional publishers are aggressively cost-cutting…it makes less and less sense.

I wish Blundell and his crew the best. But there are more and more games and more and more studios seeking success in a world of decreasing opportunities for it. The market needs to correct for the oversupply. The industry doesn’t need more games—it needs a correction.

Events were triggered in the mid-1960s that culminated in a bow wave of buyers whom consoles could be sold to 3 decades later, in the 1990s. Ten years after that, those buyers were giving rise to the opportunity for a second round of explosive growth in the market, one that would be more beneficial to the platform owners of the 2000’s, now that there were fewer competitors than there had been before.

This is a detailed discussion of the history of the gaming industry and the socioeconomics in the United States that enabled The Great Age of Affordable Gaming; an era that lasted from 2005 until 2020. And that contextualizes today’s fifth age of the gaming market’s evolution and provides reasons why and describes how we have entered The Long-Lasting, Quasi-Perpetual Bubble. The bubble that may not collapse, but will offer less stability to traditional market sub-segments, and much more greatly fragment and stovepipe the industry.

First things first; we need to level set some definitions of terms, because the internet screws these up all the time, myself included. The first key ones are disposable income and discretionary income and the difference between the two. Disposable household income is money left after taxes, used for all living expenses. Discretionary household income is the smaller amount remaining after paying taxes and essential living expenses (housing, food, utilities). Disposable is total “take-home” pay; discretionary is “fun money” for savings or luxuries.

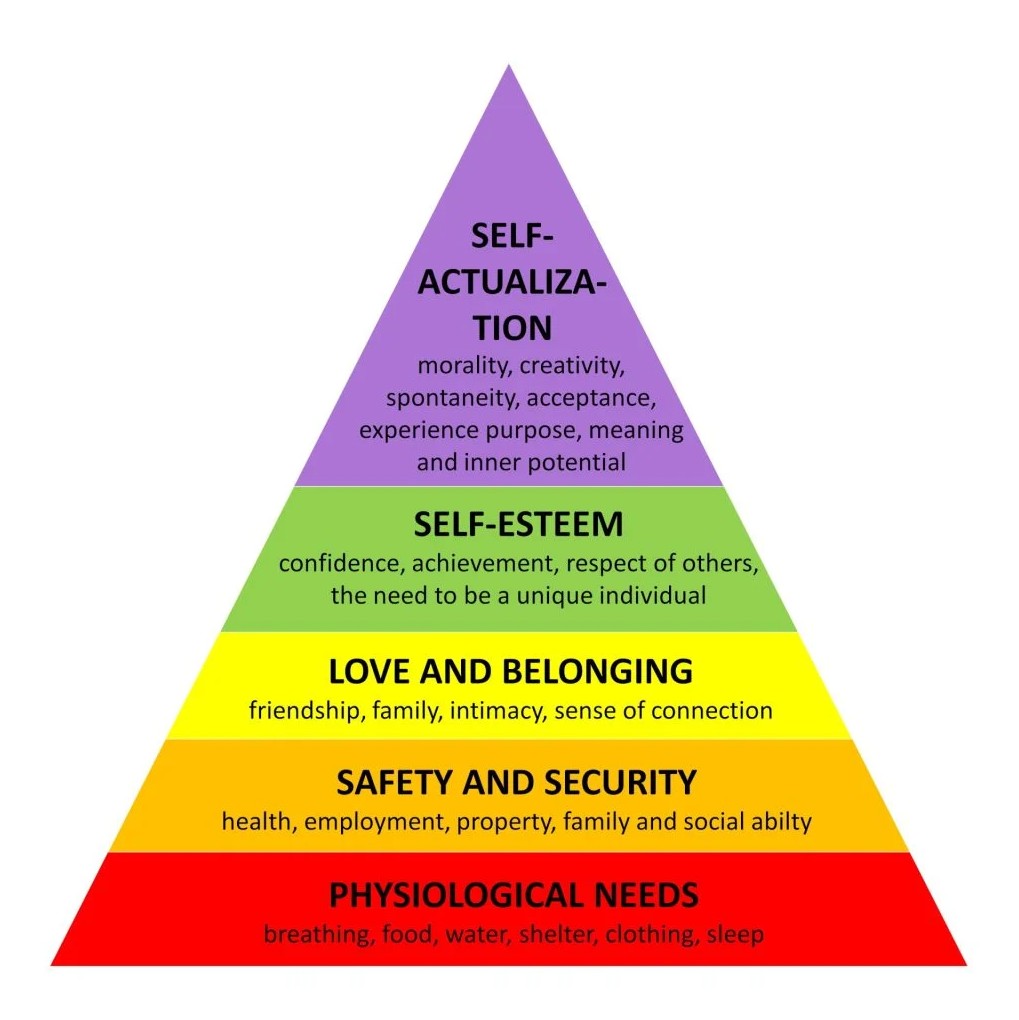

Second, we need to cover Maslow’s Hierarchy of needs, because a lot of people have it mistaken in their view that playing video games is not a luxury; Americans in particular suffer from a horrendous case of decompression sickness that warps their minds and makes them think 1st world problems are all the worlds problem. “Maslow’s hierarchy of needs is a motivational theory in psychology comprising a five-tier model of human needs, often depicted as hierarchical levels within a pyramid. Needs lower down in the hierarchy must be satisfied before individuals can attend to needs higher up.”

When we talk about things, even in America, that are entitlements that we believe all Americans should have access to, we have propped up systemic, institutionalized means that have fixed those items upon our society. A great example was when, under Obama, ISP’s were designated as common carrier services, reclassifying them as Title II services. A ruling that was overturned, but then restored in 2024. What this means, despite a ruling in 2025 that established precedent that net neutrality, a subordinate principal of making the ISPs common carriers, was overreach for the FCC, is that all Americans are entitled to internet access. Cell Carriers, in terms of mobile broadband, are considered part of the common carrier pool, but the carriers themselves are designated as a private mobile service, meaning all Americans are not entitled to cell phone service. But if you have cell phone service, you are entitled to mobile broadband.

We have also institutionalized access to art for all of society, but gaming is yet to be included in that pool. Western society and America has decided people should have universal access to certain art forms. Books. Static art…paintings and sculptures. Music. But not games yet in terms of provisioning of the hardware to access it. Your public library, a common service funded by a mix of tax sources (local, state, and federal), and therefore voted into being by the American people, provides this access. Basically anything that is provided by public libraries is a thing we have, as a society, decided people have a right to access. Ditto for most tax-funded museums.

And so, acutely, this article is primarily to discuss the affordability of gaming and how it is changing in the face of rising hardware prices, and to a lesser extent software prices, gating the access to gaming for some people. So the level-set is that gaming has always been a luxury.

It has changed in its affordability over time, being unaffordable, then affordable, and now becoming unaffordable again. But throughout that time, it has always been a luxury; a thing that is not essential or an entitlement in institutionalized terms in the United States. I use these terms with all of the requisite caveats as a thing that should be understood. “More” or “less affordable”, More affordable ” for some”, less affordable “for others”.

So let’s start the history work. How is it possible that gaming began as something unaffordable if it was cheaper? “Cheaper” is a matter of great debate, won mostly by economists who convert the dollars at the time to current-day dollars. The principles of inflation and the constantly decreasing value of the dollar means that, mostly, it will always mathematically come out as near-equal over time; meaning that, for the most part, when you adjust for inflation, gaming will always seem about the same net cost as it has always been. If anything, economically, it has been cheaper. But even if you think gaming was “more affordable” in the 70s and 80s, I think what is more important is to discuss it in terms of just who it was “more affordable” for. And then adjudicate your perception as a net of the total population.

Along the way, we’re going to continue defining (debunking) the use of terms that get twisted that actually have very specific economic definitions. Let’s first talk about what is meant to be to be “middle-class”. Being middle class generally means having a household income that is two-thirds to double the median. The U.S. median household income was approximately $83,730 in 2024. Today, economists show this bracket as typically ranging from roughly $50,000$ to $150,000+ annually, depending on location. In discussion, I typically use $170k as the upper band. It is characterized by financial stability, the ability to afford moderate luxuries (vacations, dining out), and reliance on credit for major assets like homes and cars.

Key Aspects of the Middle Class:

Income Ranges: While definitions vary, in 2023, the national middle-class household income was generally defined between roughly $53,740 and $161,220.

Cost of Living Adjustments: The definition shifts based on location and household size. For example, 2025 analysis shows in high-cost states like Massachusetts, a four-person household could need over $170,000 to be considered middle class.

Key Characteristics:

Financial Stability: The ability to save for retirement and handle unexpected expenses.

Education and Career: Often includes individuals with college degrees or those in professional/salaried roles.

Consumer Habits: Access to quality healthcare, homeowners (or aspiring homeowners), and ability to afford amenities.

SONY DSC

So when you talk about this definition, and choose to make an assertion like “gaming was more affordable in the ’70s and ’80s”, an assertion which is, inherently, based on who was in the middle class….was everyone in that pool in the ’70s and ’80s? Most decidedly not.

Two key events happened in the 1960’s. The Civil Rights Act of 1964 begat a series of US codes that were designed to level the playing field for all people in the workplace, having especially impactful results along racial and gender lines. In 1965, the Higher Education Act strengthened federal funding for HBCUs. But it also introduced the modern form of Federal Student Aid, added federal funds for continuing education, provided federal funds to recruit teachers to underserved schools (thereby raising the academic competitiveness of students within those schools), impacting admissions policies for colleges in an effort to end discriminatory practices.

Since then, a few enabling effects occurred on the path from the 1960s to the 1990s.

High School Completion: The Black high school dropout rate fell from 33% in 1968 to 5% in 2018, essentially closing the gap with the national average.

College Attainment: From 1960 to 1991, the percentage of Black males (25-29) completing at least 4 years of college rose from 12% to 18%.

HBCU Economic Mobility: HBCUs, strengthened by 1965 federal recognition, act as major upward mobility engines. Graduates from these institutions are 14.6 percentage points more likely to earn a BA than comparable peers, and 70% of their graduates reach the middle class or above.

Income Premium: Ten years after graduation, first-generation HBCU graduates have income levels on par with non-first-generation graduates.

Shift from Labor to Professional Roles: Post-1964, Black workers saw increased access to white-collar jobs, moving away from manual labor jobs where they were previously segregated.

Federal Sector Representation: In FY 2020, African American women made up 11.7% of the civilian Federal workforce, nearly twice their participation in the Civilian Labor Force (CLF).

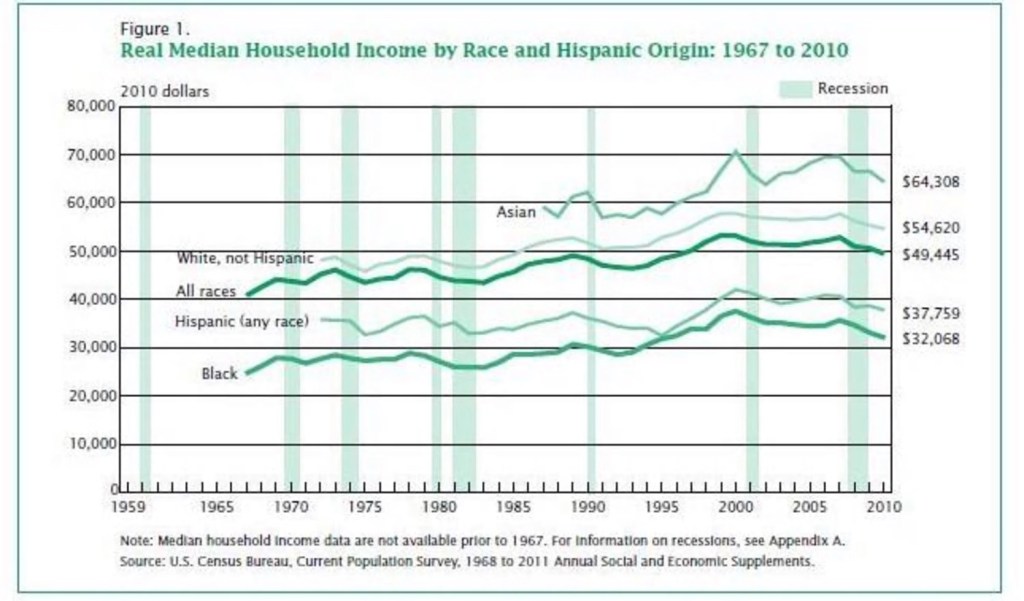

Income Growth: Real median household income for Black households has risen since the late 1960s.

Record Highs: In 2023, Black median household income reached its highest point in a generation.

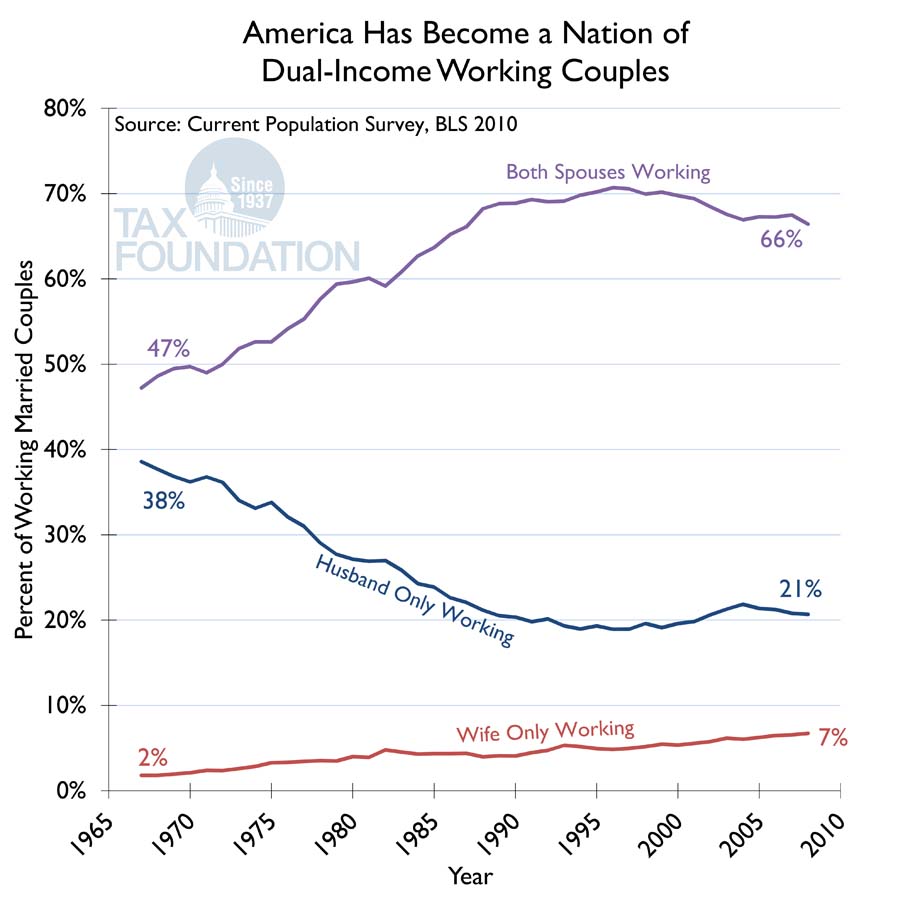

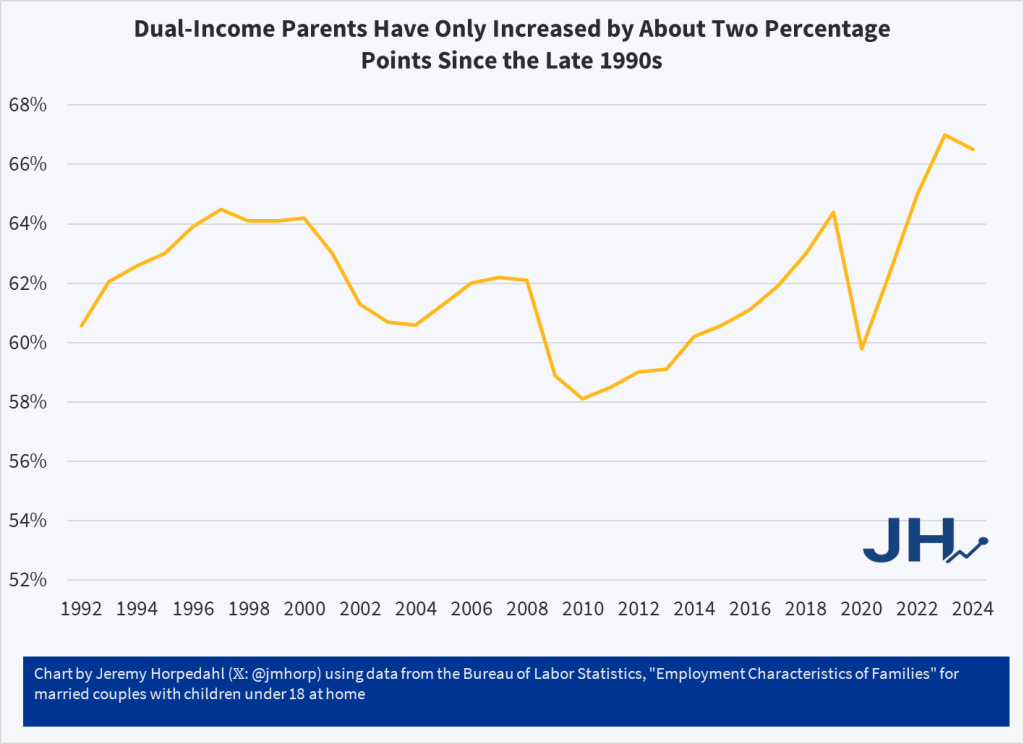

Dual-income households increased significantly between the mid-1960s and mid-1990s as more women entered the workforce. While less than half of married couples were dual-earners in the 1960s, this increased from roughly 30% of families in 1970 to over 50–60% by the 1990s. By 1994, this surge made dual-income households a common structure in the US.

1960s Context: In the 1960s, the “sole-breadwinner” household was not the strict norm, but dual-earner couples were still less than half. Data for 1967 shows 44% of married-couple families had earnings from both spouses.

The Shift: From the 1970s onwards, the trend grew rapidly. By 1994, the trend was firmly established, heading toward the 66% level observed in the following decades.

***Impact ***: By 1994, the increase in dual-income couples resulted in a higher concentration of income in the upper income quintiles, as many households had two earners.

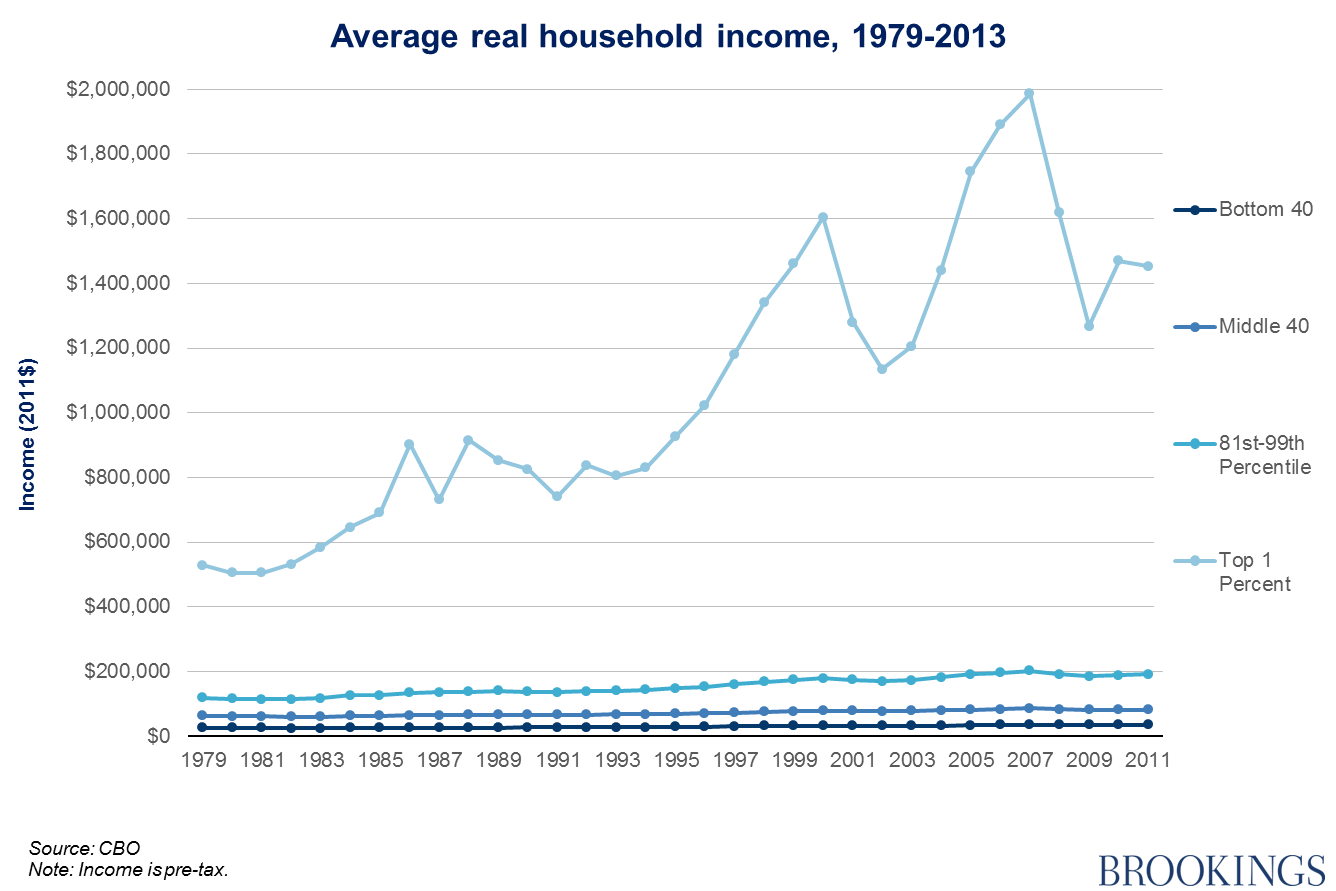

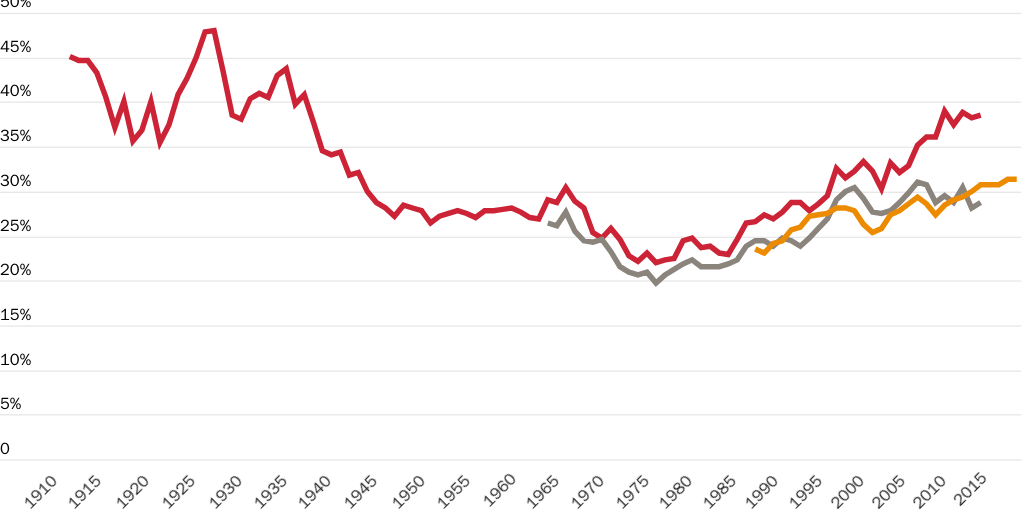

While this was occurring, a second dynamic was starting to take place beneath the surface. While it was true that there was an increase in the percentage of dual-income earning households, an increase in racial minorities and women entering the professional salaried ranks, and a modest increase in the wages of the middle-class, a secondary effect began swirling that really became a catalyst. That was a diverging hockey-stick effect altering wealth equity in the country. The really wealthy, not the middle class, but the band that we call upper-income, began accruing wealth in an uneven distribution ratio in comparison to the middle-class. In essence, the rich were getting richer, and at a rate well-exceeding the ability of the middle-class to keep up. Now, before we think “upper-income” means the Elon Musks and members of the billionaires club. Today, Upper-income households in the US are generally defined as those earning more than double the national median, starting at over $167,460 to $169,800 annually for a three-person household, according to Pew Research. More elite tiers start higher, with top 10% earners starting at $251,040+ and the top 1% at $659,060+.

So, in the 1990s, you had high median household income growth (10% over the decade), record stock market growth (Dow Jones up 309%), and a steady decline in the poverty rate (reaching 11% in 2000). The late 90s experienced a rapid productivity surge, low inflation, and a surge in household wealth. And despite the increasing divorce rate in the US, Women’s participation in the workforce grew to 60% by the end of the 1990s, with their income relative to men’s increasing. The share of high-income households increased dramatically. In 1967, only about 9% of US households earned $100,000 or more (in 2017 dollars), but by 1990 this had risen to over 15%, with continued rapid growth throughout the 1990s.

These are the conditions that led to a commensurate boom in the video games industry that began in the 1990s. The convergence of explosive growth in the combined middle-class and upper-income households that home video game consoles could be sold to; a burgeoning increasingly larger addressable market, converged and reached critical mass. While the video games market in the US would only support two set-top console competitors from 1985 – 1994, the mid-90s saw a time when the market was willing to support 3 main console competitors (Nintendo, Sega, and PlayStation), and 5 second-ring competitors, albeit for a short time (3DO, Philips CD-i, Neo Geo, Turbo Grafx, and the Atari Jaguar). There is a reason that these consoles were supported and the landscape of the console gaming market radically changed in the 1990s. It didn’t just happen by sheer chance and industry force of will.

Between 1994 and 2005, this support buckled, with the market telegraphing that it was only willing to support three console vendors. The second-ring competitors all failed out. And Sega also became a casualty of market demand (and its own mis-steps). It would be Xbox, PlayStation, and Nintendo that would create the new 3-front war. But those diverging economic hockey-sticks that started in the 90s create a new problem. The rate of increase of dual-income households had flattened out by 2005. While the upper-income households were continuing to earn more, the middle-class was barely keeping up. And so, in order to maintain industry growth, we entered The Great Age of Affordable Gaming (2005 – 2020). A time period where, whether sub-consciously or deliberately, the platform owners kept pricing relatively flat, with very little increases in hardware prices across three generations of consoles, and no increases in the stock price of the primary SKU in retail gaming software. This despite rising production costs for games.

Those diverging hockey-sticks, what was coined as the “K-shaped economy” by economist Peter Atwater in 2020 in reference to dynamics we saw during the pandemic recovery period (but has really been going on since the 1990s; it was exacerbated and accelerated by the rise of the knowledge worker in the shift in the American employment landscape since 2000), has led to an effect in the 5th Economic Age of the Games Industry. Underpinning that age are facts like “In the past five years, the top 10% of U.S. households gained more wealth than the bottom 90% combined—even after accounting for all those circa-2020 stimulus checks and wage gains.”

What also needs to be understood is that while the Upper-Income bands are garnering more of the net wealth, they are also increasing as a net percentage of all American households. Upper-income households were 14% of US households in 1971, 18% in 1991, and are now 30 – 33%. The middle-class households were 61% in 1971, 56% in 1991.

“The economics are important… But it’s how people now feel that matters most. As we see so often in history, when people feel powerless and uncertain, it impacts their political and social choices, not just what and how much they buy.” —Economist and adjunct professor Peter Atwater, speaking to W&M News.

And that is what is going on now in terms of the responses that pepper the landscape of social media with regards to the rising prices of video gaming. It is mainly about how people feel, and in that, what needs to be acknowledged and recognized is that the reactions are not everyone’s. And not just social media, but in real-world terms of how the market has, is, and will act. For the middle-classs, they are experiencing a thing called “The Squeeze”. They are experiencing an acute contraction in their earnings, largely due to rising costs for housing, healthcare, and education exceeding wage growth. While six-figure incomes were once firmly upper-middle class, they are increasingly becoming the standard for middle-class status in many U.S. states. And the buying power in that band is under siege. Meanwhile, as I’ve been saying for four years, and as corroborated by Circana data months ago, the Upper-Income households continue to spend. The Great Age of Affordable Gaming is over. Since 2020, we have entered The Long-Term Quasi-Perpetual Bubble, a 5th age in the economy of the gaming market & industry. A period of time when the industry is mostly moving forward on the support of the Upper-Income bands, with less support from the middle-class.

It is a bubble that could burst at any time. I don’t think it will. I think it will deflate a little, in very specific slices of where certain vendors operate in the market demographics. And there will be winners and losers in whose specific slice deflates, who remains afloat, and who needs to pivot, some of which you are already seeing. You can read about what that future looks like in the two articles I previously published:

“To be successful, games need to be on every platform.”

“The most successful games are multiplatform”

=> They are also the ones that tend to be cross-generational. If you’ve been playing the games that supposedly “everyone plays” while they “ignore exclusives” and believe “exclusives don’t matter”, then a persistent cross-generational state of affairs in a gen btn console HW doesn’t have the impact some have claimed today. You can think it does now, but true-up the rest of the proclamations. The gamers supposedly playing all of those games…NBA 2K, CoD, all the GAAS stuff…those players have been playing those games while “held back” by the previous gen, so people not upgrading to the PS6 won’t impact that segment of the market as something new. They already do.

=> On PC, those of us on the high-end, for time immemorial, have upgraded while being conscious that we are “held back” by PC Potato Nation; the 86% of the market. The market slice that drives consumption of older games, non-premium games, tons of GAAS…isn’t worried about performance…plays at 1080p. For the 14% who stay on the bleeding edge & current gen tech, it is a market economy we have become accustomed to and settled with. For some console players, it will be system shock; a bit of “Welcome to the suck”.

=> I see some other content creators finally getting the thing I have been talking about for years, CLV (although they don’t use this term). The battleground is the digital storefront, the console piece of HW is the primary access-point for that, you need to put it in the hands of users, and give them a reason to choose yours over another competitor’s. You can do that with differentiated content (exclusives), differentiated & competitive pricing (value), or exclusive access to a value-service.

=> I’ve also mentioned before how other consumer electronic spaces have for a long time stopped generational MSRP cuts. An iPhone or Galaxy will cost you launch MSRP the day before the new one launches. For a long time, suppliers have kept their MSRP for SKUs until they launch the new one. Those days have come to console & other world economic factors are leading to additional price increases.

=> Reality: some people and parts of the market will get priced out. On PC, people have been getting priced out of the $500 budget build that used to be viable a decade ago. The era of the $500 GPU has also ended (the GTX 1070 launched w/an MSRP of $379, $449 for the Founders Edition). On PC, the “cross-gen” market economy and value-prop decision factor is an engrained way of life.

None of this is to say anything is fair, justified. It is to state conditions of dynamics in adjacent markets. People will have to make choices and decisions. Maybe next-gen there will be an actual battle btn the market demo that puts a priority on quality vs the demo that puts a priority on low-cost of access. In that world, maybe value-props like Smart Delivery, Game Pass, Play Anywhere, and being able to access your games on a mobile device through the Cloud will make a bigger difference. The console cross-gen split might start to look more like PC. If so, I reckon the ones who decide to stay on the edge of tech in consoles will do the same as high-end PC players…make decisions about where they want to play, and make peace with that decision.

As I wrote earlier this week, the gaming industry has been on a perpetual, long-term bubble for the last 5 – 7 years. If the blister pops, there will be more damage. But it also seems that the blister is not likely to heal on its own. At least not quickly and without the death by 1000-cuts approach we are experiencing. There needs to be a market correction. And “the answer” to that is not less powerful HW, although lower-priced SKUs will be part of the mix. The unfortunate key answer is fewer games. And sad to say fewer studios. Over-saturating inventory with product people don’t buy, especially in the face of rising HW prices, doesn’t make sense.